.jpg#keepProtocol)

.jpg#keepProtocol&description=The+Way+forward+for+Cashless+Funds+%5B%2B+How+to+Get+Ready+With+Affordable+Tools%5D){kind=link}

20 years in the past, it was onerous to think about a world the place money did not exist. However with the rise in reputation of cashless cost strategies, a society with out money may quickly turn into a actuality.

The COVID-19 pandemic is one main catalyst for the shift. To reduce direct contact, individuals gravitated in direction of cost strategies that did not require the usage of bodily cash, like financial institution playing cards and cost apps.

On this article, you may study what specialists take into consideration the way forward for cashless funds, cost strategies on the horizon, and firms which are already making the change.

Cashless Funds In the present day

Corporations Testing Cashless Experiences

Easy methods to Set Up Cashless Funds

Undertake Cashless Cost Strategies

Cashless Cost Predictions

The worldwide transition to cashless cost strategies is going on in a short time. Consultants consider that earlier than lengthy, we’ll be residing in a cashless society. Actually, some nations are already working to fully eradicate money from their economies.

Sweden has diminished the quantity of money in circulation by 50% during the last decade.

Based on the European Funds Council, conventional money transactions made up simply 1% of Sweden’s gross home product (GDP), and ATM money withdrawals are steadily declining by 10% every year. The Swedish Central Financial institution lately said that solely 9% of the nation’s inhabitants makes use of money for transactions proper now.

Now, analysts predict that Sweden will turn into the primary cashless nation on the earth by 2023.

In PwC’s 2025 & Past: Navigating the Funds Matrix, PwC explored the continuing transition from cash-based to cashless cost strategies, the event of digital economies, and the affect of recent cost traits.

Listed below are a few of the cashless cost predictions within the report:

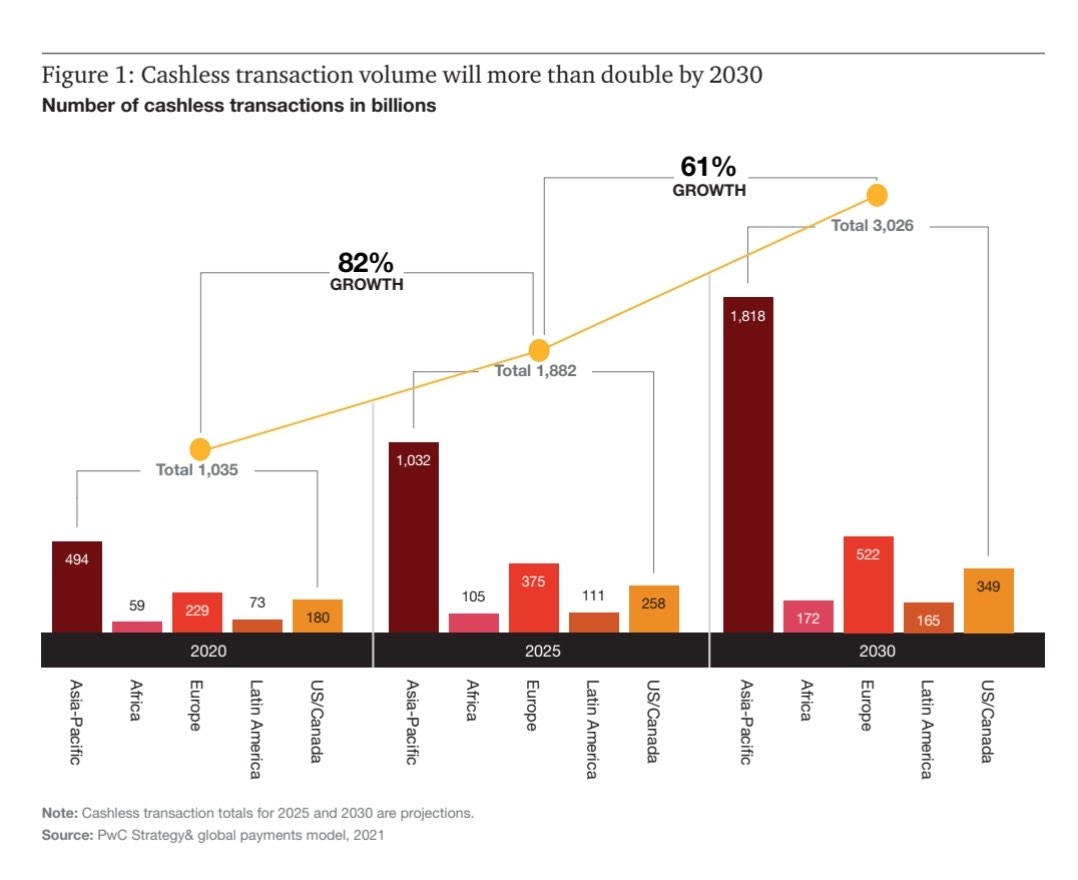

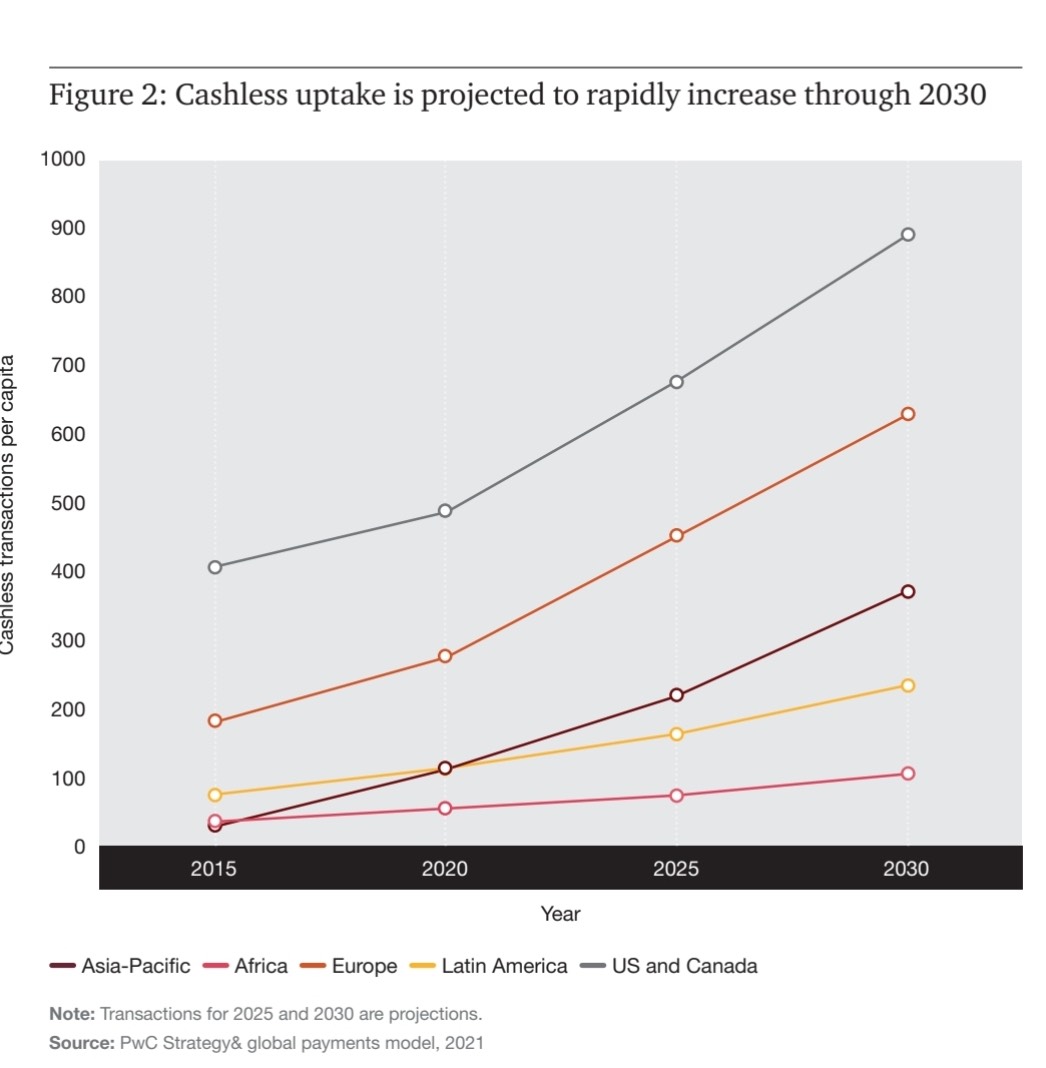

- Cashless transactions will develop quickest in Asia-Pacific, rising by 109% from 2020 to 2025, after which by 76% from 2025 to 2030, adopted by Africa and Europe.

- International cashless cost volumes are set to extend by greater than 80% from 2020 to 2025, and to nearly triple by 2030.

- 89% of respondents agreed that the buyer shift from bodily shops to on-line shops will proceed to extend, requiring important funding in on-line cost options.

- Digital wallets will account for greater than half of all e-commerce funds worldwide by 2024.

Cashless Funds In the present day

Listed below are a few of the cashless and contactless cost strategies which are rising in reputation. You may already use a few of these funds whenever you go to the shop. Consultants predict companies will supply many of those cost strategies shifting ahead.

Credit score and Debit Playing cards

Credit score and debit playing cards are probably the most steadily used cashless cost strategies on the earth proper now. They’re a fast, safe, and handy technique of cost.

However the usage of banking playing cards has begun to say no in favor of cell wallets and cost apps. In 2021, bank cards and debit playing cards accounted for 21% and 13% of world e-commerce cost strategies, respectively. By 2025, the usage of bank cards is predicted to fall to 19%, whereas debit playing cards will stay secure at 13%.

In case you personal a enterprise, this doesn’t imply you need to fully forgo banking playing cards and begin utilizing cell wallets as an alternative. By 2025 (and past), many individuals will nonetheless depend on banking playing cards to make funds, particularly now that banks are issuing playing cards enabled with Faucet to Pay know-how.

Savvy companies settle for each banking playing cards and cell wallets as viable cost strategies.

Cellular Wallets and Cost Apps

Cellular wallets, or digital wallets, are monetary functions that run on cell units. These apps securely retailer your cost card data to be able to pay for objects on-line or in-store with out having to hold your playing cards round. All you’ll want to provoke transactions is your smartphone/smartwatch and a superb web connection.

Examples of cell wallets and cost apps embody:

- Apple Pay

- Google Pay

- Samsung Pay

- PayPal

- Venmo

- CashApp

- AliPay

Digital wallets are extraordinarily common right this moment, and also you possible use them typically. Ian Wright, the founding father of Service provider Machine, believes that the recognition of cell wallets will solely develop sooner or later.

“Merchandise like Apple Pay and Google Pay will definitely turn into extra ubiquitous, which can give Apple and Google the chance to disrupt Visa and Mastercard,” Wright says.

That is true. Knowledge from FIS International Funds Report 2022 reveals that by 2025, cell wallets can be used for 53% of e-commerce transactions worldwide — rising from 49% in 2021. For international point-of-sale (POS) transactions, the usage of digital wallets is predicted to rise from 29% in 2021 to 39% in 2025.

FIS discovered that individuals have began utilizing digital wallets for funds greater than they use their playing cards. E-wallets are anticipated to outgrow different POS cost strategies and attain a 36.8% share — over $22.7 trillion.

Cryptocurrency

At this 12 months’s Tremendous Bowl recreation, audiences had been proven a intelligent 60-second advert from Coinbase, a platform for getting and promoting cryptocurrency. This advert got here within the type of a QR code that, when scanned, took individuals to Coinbase’s web site the place they provided free Bitcoin price $15 to new signups (for a restricted time).

Not lengthy after the advert aired, Coinbase’s app crashed from the inflow of site visitors from the Tremendous Bowl.

That goes to indicate simply how mainstream cryptocurrency is — particularly Bitcoin, which is the usual digital foreign money for cell funds.

Bitcoin does not require further charges or intermediaries to maneuver from a shopper to a service provider. Apps like Coinbox implement a POS performance to make the cost course of simpler for each companies and prospects.

Cost apps like PayPal have additionally began supporting crypto buying and selling and funds on their apps. Main firms like Microsoft and Expedia are additionally accepting crypto funds.

The crypto market is unstable, fluctuating steadily. This cost technique is probably not the most suitable choice for small-to-medium-sized companies proper now. But when the market stabilizes, it may very nicely be.

Central Financial institution Digital Foreign money

Central Financial institution Digital Currencies (CBDCs) are digital tokens issued by a rustic’s central financial institution to signify the digital type of that nation’s foreign money. This digital foreign money has the identical worth as fiat (bodily) cash.

The primary purpose of CBDCs is to supply privateness, monetary safety, accessibility, transferability, and comfort to companies and customers — particularly people who have restricted entry to banks. CBDCs additionally purpose to scale back the dangers of utilizing digital currencies (aka cryptocurrency) of their current, unstable type.

“If CBDCs are designed prudently, they’ll probably supply extra resilience, extra security, larger availability, and decrease prices than non-public types of digital cash,” IMF Managing Director, Kristalina Georgieva, mentioned in her 2022 speech on the Atlantic Council in Washington D.C.

“That’s clearly the case when in comparison with unbacked crypto belongings which are inherently unstable,” she says. “And even the higher managed and controlled stablecoins is probably not fairly a match in opposition to a secure and well-designed central financial institution digital foreign money.”

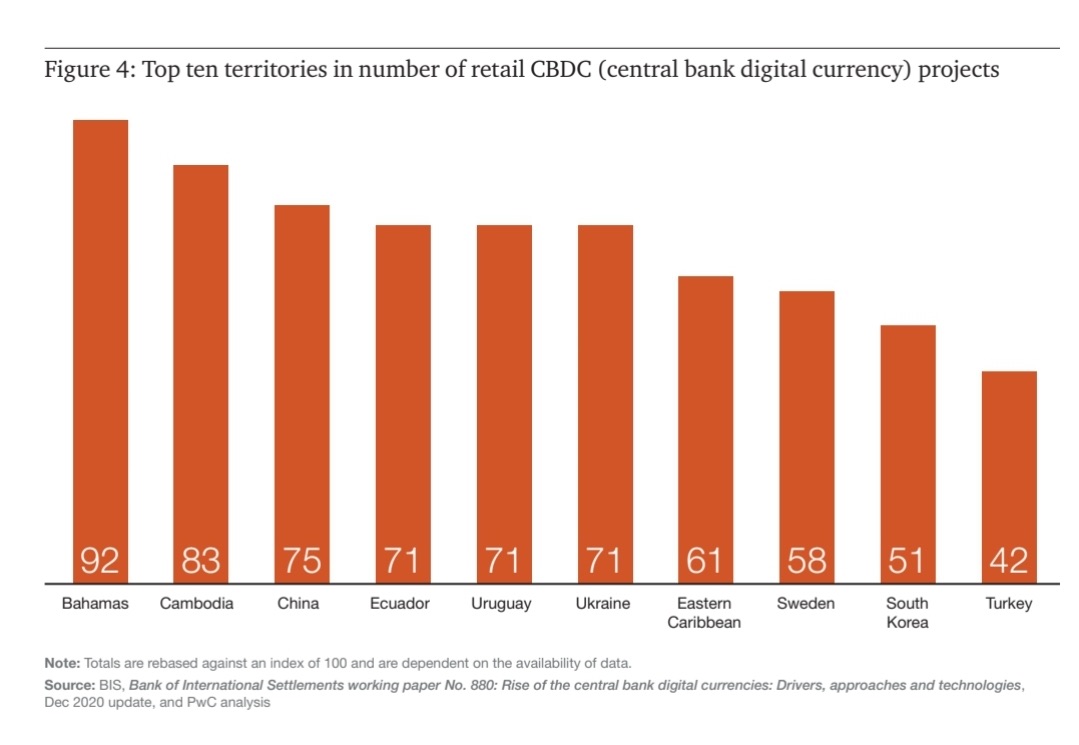

Proper now, ten nations and territories have launched CBDCs:

- Nigeria

- Jamaica

- Grenada

- The Bahamas

- Dominica

- Antigua and Barbuda

- Montserrat

- Saint Lucia

- St. Vincent and the Grenadines

- St. Kitts and Nevis

About 105 different nations, together with the U.S. and the U.Ok., are nonetheless investigating CBDCs and the way they have an effect on present monetary networks.

QR Codes

Fast Response codes, or QR codes, are machine-readable barcodes that retailer data. This code consists of distinctive black and white pixels in a square-shaped grid.

To make funds through QR codes, an individual has to scan the code displayed by the service provider with their cell system. Then, customers put within the quantity they should pay and submit.

Apple launched QR code scanners in smartphones in 2017. Since then, most — if not all — different smartphone manufacturers have included them into their fashions. And now, QR code funds are probably the most environment friendly and common cashless cost strategies on the earth.

The numbers replicate this. In 2020 through the pandemic, 1.5 billion individuals used QR codes to make a cost, in accordance with Juniper Analysis. The agency additionally predicts that 30% of all cell customers will use QR codes by 2025.

This cost technique is a safe different to money transfers. Plus, companies can course of transactions with out having to purchase conventional cost {hardware}. All they should do is ready up QR codes that may take prospects to their net cost type.

ACH Financial institution Transfers

An ACH switch is an digital cost made between financial institution accounts by the Automated Clearing Home (ACH) community.

This cost technique is likely one of the hottest sorts of financial institution transfers and is used for B2B direct deposit and computerized invoice funds. Actually, 93% of People use ACH transfers to obtain their salaries and pensions.

In 2021, the amount of cash transferred by the ACH was over $8.89 trillion. That’s greater than the quantity transferred through checks and wire transfers.

All banks in the US assist ACH funds. Now, cost processors like PayPal, Stripe, and Sq. additionally assist this cost technique.

All that you’ll want to make or obtain an ACH cost is a working checking account and routing quantity. Transfers made by this route sometimes take 3-4 enterprise days to finish.

ACH funds have decrease processing charges than bank cards. So if in case you have purchasers that pay you recurring charges or workers that you just pay each month, ACH transfers are an effective way to do this with out incurring a loss. That is particularly good for companies in industries like authorized, healthcare, training, property administration, and subscription-based providers.

Brick-and-mortar retail companies shouldn’t use ACH funds for POS buyer transactions. ACH transfers require a checking account and routing quantity and many consumers don’t know their banking data off-hand.

Purchase Now, Pay Later

Purchase Now, Pay Later (BNPL) is a cost technique that permits prospects to buy costly objects on credit score and pay in installments over time. It’s a kind of mortgage, besides you don’t should pay curiosity for those who make your funds on time and in full.

The prospect of having the ability to make a number of interest-free funds over time can encourage consumers to purchase extra, which leads to extra income for distributors. A research by McKinsey confirmed that 29% of BNPL customers would have made a smaller purchase or wouldn’t have purchased in any respect if this cost choice wasn’t out there.

Banks like Chase and a few bank card firms supply cardholders the chance to purchase objects and pay for them later. Apps like Afterpay (acquired by Sq.) and PayPal have additionally jumped on the bandwagon.

In 2021, BNPL accounted for 2.9% of world e-commerce transactions (a $157 billion worth). Juniper’s analysis predicts that this worth will develop 5.3% (or to $438 billion worth) by 2025.

Corporations which are already testing new cashless experiences

Amazon

In early 2020, e-commerce large Amazon introduced its new contactless cost know-how, Amazon One. This is the way it works: Customers go to a point-of-sale station in sure places to hyperlink their palms and cost playing cards to Amazon One. As soon as they’ve carried out that, all they should do at future checkouts is hover their hand over a scanner to pay for his or her objects.

The reasoning behind that is easy. Your palm is made up of tiny, largely undetectable options which are distinctive to you. The Amazon One system, nonetheless, can learn and acknowledge these options.

The system makes use of laptop imaginative and prescient algorithms and proprietary imaging to seize and encipher a picture of your palms. This manner, it creates a singular palm signature that it may possibly acknowledge each time you utilize the system.

As of September 2021, Amazon rolled out this new cost technique to over 65 Complete Meals shops in California. This large rollout actually helps Amazon in its effort to modernize retail procuring and make it simpler for patrons to make funds.

Walmart

In December 2021, Walmart quietly filed a number of new emblems that point out that it plans to make and promote digital objects, together with toys, electronics, self-care merchandise, and residential décor within the metaverse. Mainly, Walmart desires to create its personal cryptocurrency and non-fungible token (NFT) collections.

Quick ahead to September 2022 and Walmart introduced that they’re launching two digital experiences — Walmart Land and Walmart Universe of Play — in Roblox, a gaming platform.

These experiences will characteristic completely different video games, a blimp that drops toys, a music pageant with common artists, and a retailer of digital merchandise (referred to as “verch”) that matches Walmart’s bodily and on-line stock.

Walmart’s Chief Advertising Officer, William White informed CNBC that Roblox is presently a testing floor for Walmart because it considers working within the metaverse and past. He additionally mentioned that the way in which COVID-19 all of the sudden reworked individuals’s procuring habits and on-line engagement prompted Walmart to start out experimenting with new methods to achieve consumers — particularly Gen Zs.

On income, White famous that Walmart will not make any cash from these newly launched digital experiences for now. But when issues work out nicely, they may make cash by partnering with different manufacturers or by turning individuals’s immersive experiences into real-life retailer visits or on-line purchases.

Albertsons

One more retail large is experimenting with cashless funds. For Albertsons, it is I-powered self-checkout carts.

These carts are made by Veeve, an organization based by two ex-Amazon engineers, and so they purpose to make in-person procuring smoother, particularly in short-staffed shops. These carts use cameras and sensors to scan objects that consumers choose, evaluate merchandise, and make personalised suggestions through a small on-cart display screen. These carts additionally construct 3D fashions of all of the merchandise within the retailer, in order that it may possibly acknowledge this stuff over time with out the client scanning them.

What’s extra, you do not want to take a look at whenever you use this cart. After procuring with Veeve carts, individuals will pay for his or her objects by inserting or tapping their card with out ever going to the checkout line.

In November 2021, Albertsons began testing these carts at two of its shops in California and Idaho. Now, they’re increasing and including the carts to extra shops.

Apple

In June this 12 months, Apple launched the Faucet to Pay know-how on iPhones. Based on Apple, this new tech will allow hundreds of thousands of US retailers — from solopreneurs to mega-retailers — to simply settle for contactless credit score and debit playing cards, Apple Pay, and different cell wallets through a faucet of an iPhone. No cost terminal or further {hardware} wanted.

After an individual is finished procuring, the service provider will inform the client to carry their iPhone to pay with their contactless card, Apple Pay, or different digital pockets close to the product owner’s iPhone. With the faucet of a button, the cash strikes from the client to the service provider by near-field communication (NFC) know-how.

Apple is partnering with cost apps like Sq. and Stripe to make the Faucet to Pay on iPhone characteristic out there on their platforms. This characteristic will solely work with contactless credit score and debit playing cards from common cost networks, together with Visa, MasterCard, American Specific, and Uncover.

Be aware: Faucet to Pay characteristic solely works on the Telephone XS or newer. Older iPhone fashions do not assist this characteristic.

In October this 12 months, Google introduced that it has partnered with Coinbase to simply accept cryptocurrency funds for its cloud providers.

Each Google and Coinbase wish to diversify their enterprise fashions and increase their choices. For Google, accepting crypto funds will give them entry to fast-growth firms within the Web3 area. These firms would pay for Google’s cloud providers by Coinbase — a platform that trades ten completely different digital currencies, together with Bitcoin, Ethereum, Litecoin, and Dogecoin.

As digital funds are available, Coinbase will take a lower of the charges, which is able to function a separate income stream that is not immediately associated to retail buying and selling charges.

Easy methods to Set Up Cashless Funds

With the rising reputation of cashless cost strategies, companies that wish to keep related sooner or later should arrange versatile cost strategies. Listed below are some methods you may put together.

1. Contemplate the cost strategies your prospects want.

Not all companies are the identical. In case you’re a small enterprise, there is a good likelihood you will not be capable to use the identical cost strategies as massive enterprises just because it isn’t essential.

The easiest way to know for certain which cost strategies you need to settle for is by figuring out your prospects’ cost preferences and implementing these choices.

For instance, in case your prospects like utilizing their playing cards to pay, arrange a POS terminal. If lots of your prospects have contactless cost playing cards or use iPhones lots, you may settle for funds through the Faucet to Pay know-how. But when they do not carry playing cards in any respect, there are different choices you may supply, like digital wallets or QR codes.

An vital factor to contemplate is that your prospects’ cost preferences could differ by age, location, and different demographic elements. So it is best to supply completely different cost choices so that you just cater to all of your prospects’ wants.

2. Use a cost processor.

To simply accept debit card and bank card funds, digital pockets funds, and ACH transfers, companies should companion with a cost processor that complies with Cost Card Business (PCI) requirements. Cost processors are third-party distributors (or apps) that handle monetary transactions by mediating between the service provider and prospects concerned.

These apps make sure that a buyer has sufficient funds to pay for an merchandise and securely transfer the cash from the client’s account to the product owner’s within the blink of a watch.

Widespread cost processors embody:

- Sq.

- Clover

- Stripe

- Stax

- Cost Depot

- PayPal

- Payoneer

Along with cost processing, a few of these apps supply service provider accounts and cost gateways.

When choosing the proper cost processor for your small business, look out for the next:

- The form of funds the processor accepts.

- The charges the processor prices per transaction.

- What platform transactions can happen.

3. Provide Purchase Now, Pay Later.

It has been confirmed that retailers that provide a Purchase Now, Pay Later (BNPL) choice to their prospects are more likely to get extra gross sales.

Between 2020 and 2021, the speed of American customers utilizing the BNPL cost choice elevated by 80%. Of these customers, 40% had been millennials, and Gen Z customers are rapidly catching up. So for those who’re making an attempt to increase your buyer base to incorporate youthful individuals, BNPL may help you get there.

This cost technique works exceptionally nicely for e-commerce shops to achieve new prospects, get extra conversions, and improve common order worth (AOV).

Some dependable BNPL suppliers embody:

- Affirm

- AfterPay

- Klarna

- Stripe

4. Set up a commerce-powered CRM.

Image this: You might have a buyer who’s ready so that you can ship an bill to their mailbox earlier than they’ll mail you again a examine for an merchandise they purchased. As they waited in your bill, they determined to do a trial purchase of the identical merchandise out of your competitor. As a result of your competitor affords the Faucet to Pay choice, the client was capable of pay for the merchandise in a number of seconds.

Which firm do you assume the client would wish to work with subsequent time: you or the competitor?

To stop a state of affairs like this, use a CRM platform with cost gateway integration. HubSpot is a good instance of this.

Contained in the HubSpot CRM is a local funds device that streamlines your total gross sales course of to be able to receives a commission early, tackle extra prospects/purchasers, and develop your small business. HubSpot’s funds device means that you can ship your prospects quotes or cost hyperlinks, after which they pay you. No want for paper checks.

If the funds are recurring — like on-line subscriptions — you may merely automate the method as an alternative of sending quotes to prospects each month. HubSpot funds device additionally offers your prospects the pliability to make transactions every time and nonetheless they need on the CRM.

This vastly boosts your buyer expertise and helps you preserve your relationship along with your prospects long-term.

Undertake Cashless Cost Strategies

The elevated use of cashless funds has revolutionized the way in which individuals do enterprise world wide. From grocery shops to eating places and on-line shops, many companies now supply cashless transactions.

If you’d like your small business to remain afloat throughout this alteration, you’ll want to begin accepting a wide range of cashless cost strategies. This manner, your prospects aren’t restricted of their choices, and you may accumulate funds speedily and securely.