{kind=link}

No one is having fun with this inventory market. Perhaps not the worst ever…however undoubtedly not numerous enjoyable. So let’s speak about what’s making the S&P 500 (SPY) fall decrease and decrease. And lets speak about what lies about what traders ought to do know to excel within the weeks and months forward. Learn on under for the complete story.

I’ve at all times mentioned that an unsure and risky market is absolutely the worst. Sure…even worse than a bear market.

That is as a result of with a bear market there’s a clear pattern that you would be able to lean into. Similar to shopping for inverse ETFs to earn money because the market declines.

However a risky vary sure market, comparable to this one, is only a pure headache for traders. Lots of whom are simply giving up as could be seen in lots of metrics of inventory analysis exercise and buying and selling volumes.

The bottom line is understanding the character of the present volatility and what seemingly comes on the opposite facet. Appreciating that’s the easiest way to align your portfolio now for positive factors within the weeks and months forward. That will likely be our focus as we speak.

Market Commentary

First, the inventory rally as much as 4,600 for the S&P 500 (SPY) in late July was simply too excessive given the muted earnings development because of the Fed’s hawkish insurance policies to convey inflation again to the two% goal. In order that was a pure time for a spherical of revenue taking and sector rotation earlier than the following leg increased.

However simply as shares appeared able to bounce…bond charges began to blow up increased. Not due to the Fed as they have not raised charges shortly. Moderately due to different dynamics at play that we’ll merely describe as Charge Normalization. (Extra on that subject on this commentary).

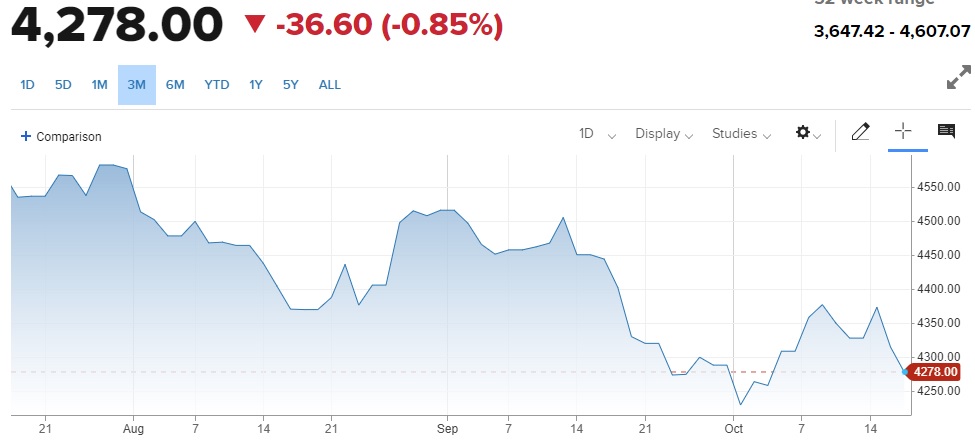

This dynamic has led to the unattractively risky, vary sure market you see within the 3 month chart under:

Sure, one might say this can be a case of decrease highs and decrease lows. And thus probably a bearish sign.

Nonetheless, with the S&P 500 nonetheless above the 200 day transferring common and 20% above the earlier bear market low…then technically nonetheless bullish.

The explanation I’m not notably involved about extra draw back is due to the present energy of the financial system. Certain, you may parade out a statistic right here or there that exhibits weak spot. That’s the reason we’re going to talk about the broadest measure of well being…that being GDP.

The GDPNow mannequin from the Atlanta Fed stands at +5.4% for Q3 whereas the Blue Chip Economist Consensus at 3.5% (seemingly extra on course). We are going to know for positive subsequent Thursday 10/26. Pardon me however there may be simply no method to have a look at these revered estimates and really feel bearish.

Maybe much more necessary than the GDP report subsequent week is the PCE Inflation studying that will get launched alongside facet of GDP. Because the Fed has said many instances over their studying of Core PCE is their most well-liked technique of studying the state of inflation. That’s anticipated to drop from 3.7% to three.1% which is transferring ever nearer to the two% goal of the Fed.

The above explains why traders at the moment are 92% positive the Fed will maintain charge regular for a second straight assembly on November 1st. Observe {that a} month in the past there was over a 30% expectation of a charge hike on the best way in November.

This all appears to fly within the face of the current discussions of upper bond charges disrupting the inventory market. I talked about that in nice element in my final commentary.

Warning: Buyers Put together for “Sea Change”

The essential story is that charges had been artificially suppressed by the Fed. In order their insurance policies modified, with much less manipulation to decrease charges, then charges are rising increased. What actually is a normalization of charges which resets the bond vs. inventory investing equation.

My sense is that 5% on the ten yr Treasury (which we’re touching now) will likely be some extent of resistance for traders. Most definitely will contact it…in all probability a smidge increased…then issues consolidate round and even underneath 5% for some time. If true, then much less motive to hit the promote button for shares particularly with the financial system trying so sturdy at the moment.

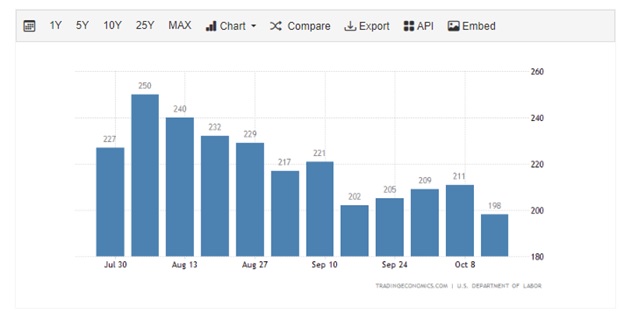

Most individuals are ready for employment image to lastly buckle as an indication the financial system is prepared for a downturn. Nonetheless, one of the best ahead trying indicator or the unemployment charge is the weekly Jobless Claims report. The nearer that will get to 300K…the extra seemingly that the unemployment charge is able to rise. Nonetheless, as you will notice within the chart under this indicator is definitely getting more healthy. That features Thursdays dip underneath 200K.

So if there isn’t a recession on the horizon. And traders are simply adjusting to this Charge Normalization, then there might certainly extra volatility forward. However past that part most indicators level bullish.

WHEN can we emerge into that subsequent bull run increased?

Unknown and unknowable at the moment. But I sense that after traders see charges stage out or pull again…then shares will likely be again in vogue as soon as once more.

DO NOT EXPECT a roaring bull market. Larger charges will result in a decrease earnings development surroundings which mutes inventory returns. Gladly these with a bonus will be capable of simply prime the modest returns of the S&P 500.

Sure, we’ve such a bonus with our POWR Rankings. Extra on these prime picks within the subsequent part…

What To Do Subsequent?

Uncover my present portfolio of seven shares packed to the brim with the outperforming advantages present in our POWR Rankings mannequin.

Plus I’ve added 5 ETFs which can be all in sectors nicely positioned to outpace the market within the weeks and months forward.

That is all primarily based on my 43 years of investing expertise seeing bull markets…bear markets…and all the pieces between.

If you’re curious to study extra, and wish to see these 12 hand chosen trades, then please click on the hyperlink under to get began now.

Steve Reitmeister’s Buying and selling Plan & Prime Picks >

Wishing you a world of funding success!

Steve Reitmeister…however everybody calls me Reity (pronounced “Righty”)

CEO, StockNews.com and Editor, Reitmeister Complete Return

SPY shares had been buying and selling at $423.52 per share on Friday morning, down $2.91 (-0.68%). 12 months-to-date, SPY has gained 11.97%, versus a % rise within the benchmark S&P 500 index throughout the identical interval.

In regards to the Writer: Steve Reitmeister

Steve is best recognized to the StockNews viewers as “Reity”. Not solely is he the CEO of the agency, however he additionally shares his 40 years of funding expertise within the Reitmeister Complete Return portfolio. Be taught extra about Reity’s background, together with hyperlinks to his most up-to-date articles and inventory picks.

The put up The Worst Inventory Market Ever? appeared first on StockNews.com